Adjustable-price mortgage loans (ARMs) can help to save borrowers a lot of money during the interest rates more than the newest brief so you’re able to typical identity. But if you is actually holding you to if it is going back to the fresh interest rate to help you reset, you can deal with a higher month-to-month home loan statement. That’s great as much as possible manage it, but if you are like a good many Us citizens, an increase in extent you pay every month is likely becoming hard to swallow.

What is an adjustable Price Financial?

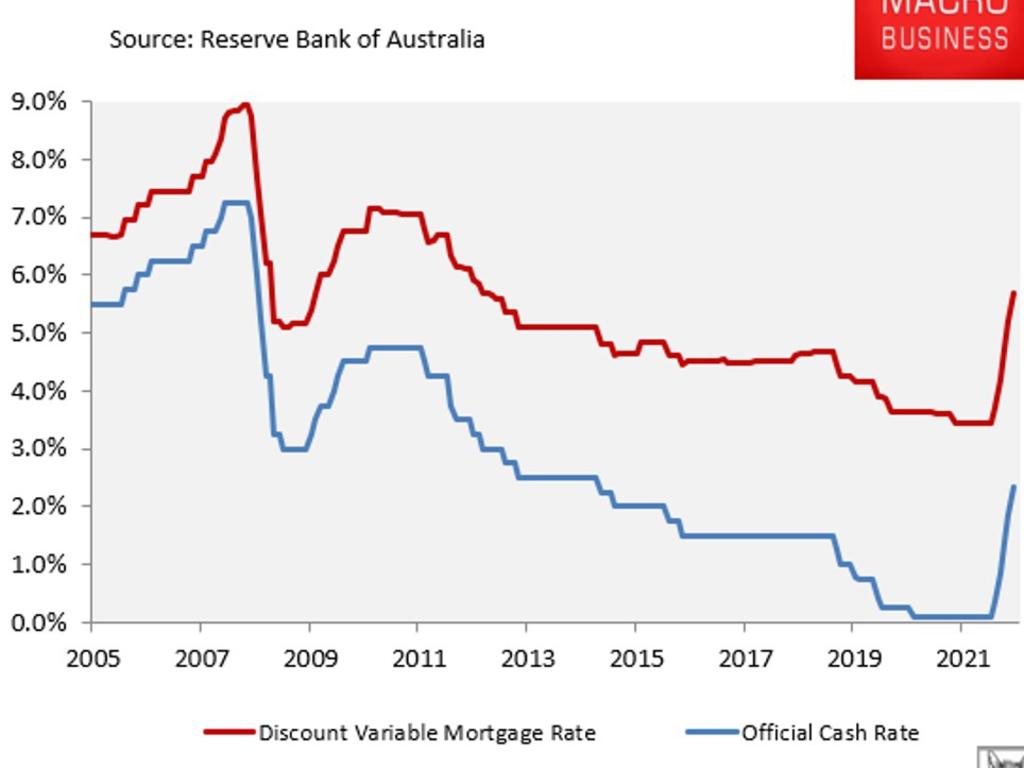

Look at this: Brand new resetting from variable-rates mortgage loans in the economic crisis explains as to the reasons, partly, so many people was pressed towards foreclosures or had to sell their houses basically transformation. Following the casing meltdown, of several economic planners put adjustable-speed mortgages on risky classification. Given that Arm has gotten a bum hiphop, it is not a bad home loan equipment, provided borrowers understand what he or she is getting into and you can what will happen when a varying-rate mortgage resets.

Key Takeaways

- An adjustable-rates financial (ARM) is a kind of mortgage where in fact the rate of interest applied toward a fantastic harmony varies on lifetime of the mortgage.

- Whenever pricing go up, Arm consumers should expect to blow higher monthly mortgage payments.

- The Arm rate of interest resets towards the a pre-place schedule, have a tendency to yearly otherwise semi-a-year.

- Which have varying-rates mortgage hats, you can find restrictions set on how much cash the interest prices and you can/or money is increase per year or over the new life of the borrowed funds.

Interest Alter which have an arm

To obtain a master about what is actually shop to you with an adjustable-speed home loan, you initially have to understand how the merchandise work. Which have an arm, borrowers lock in an interest rate, always a decreased you to, for an appartment time frame. When the period figure closes, the borrowed funds rate of interest resets so you’re able to whatever the prevailing rate of interest is. The first months where in fact the rates does not alter selections anyplace regarding half a year so you can 10 years, according to Federal Home loan Home loan Corporation, or Freddie Mac computer. For most Arm items, the rate a debtor will pay (in addition to number of the new payment) can increase substantially later in the loan.

From the first low interest, it could be popular with borrowers, for example individuals who try not to intend to stay in their homes to have too-long otherwise that happen to be experienced enough to re-finance if the focus rates increase. Nowadays, with rates of interest hanging within listing lows, consumers who had a changeable-price financial reset otherwise adjusted didn’t discover too big a reversal in their monthly obligations. But which will transform depending on how much and how rapidly the fresh Government Put aside brings up their standard rate.

Know Your Modifications Several months

To help you determine whether an arm is an excellent match, individuals must know particular rules regarding this type of financing. Essentially, the latest modifications months ‘s the months between rate of interest transform. Just take, for example, an adjustable-price mortgage who has an adjustment period of 12 months. The loan product would-be called a-1-year Case, therefore the interest-which means that new month-to-month mortgage payment-carry out changes after from year to year. If your modifications period was three years, it is called an effective step three-year Case, and price create changes every three-years.

There are also certain hybrid items like the 5/1 year Arm, that gives you a predetermined rates to the earliest five years, and then the pace adjusts after from year to year.

See the Basis for the interest rate Change

Plus focusing on how often your Sleeve tend to to change, individuals need certainly to comprehend the reason behind the change on interest rate. Lenders ft Case cost on the certain indexes, with preferred being the one-seasons constant-maturity Treasury ties, the expense of Financing Index, therefore the prime speed. Before taking out an arm, make sure to inquire the lending company and this list might possibly be used and you can take a look at how it has fluctuated prior to now.

One of the largest threats Arm borrowers deal with whenever the loan adjusts is commission treat when the month-to-month mortgage payment rises considerably by speed changes. This can end in adversity toward borrower’s region whenever they cannot manage to improve the latest fee.

To get rid of sticker shock of happening to you, make sure to stick to greatest of interest pricing since your modifications period means. With respect to the Consumer Financial Safety Board (CFPB), mortgage servicers have to give you a quote of the new commission. If your Arm was resetting the very first time, one to estimate are going to be taken to your seven to eight days up until the changes. In case your loan have modified prior to, you’ll be informed 2 to 4 months beforehand.

In addition to this, into very first alerts, lenders ought to provide choice you could speak about if you’re unable to afford the the newest rates, in addition to information about how to make contact with an effective HUD-accepted houses counselor. https://clickcashadvance.com/personal-loans-nj/windsor/ Once you understand in advance just what the new payment is about to end up being provides you with for you personally to plan for it, look around for a much better loan, otherwise score let determining exactly what your choices are.

The bottom line

Taking on a variable-speed mortgage doesn’t have to be a dangerous function, if you know very well what happens when your own home loan interest speed resets. As opposed to repaired mortgage loans for which you pay the same interest rate more the life span of your loan, which have an arm, the pace vary over time of time, and perhaps, it may rise notably. Understanding in advance exactly how much more you are able to are obligated to pay-or may are obligated to pay-every month can possibly prevent sticker surprise. More important, it assists be sure to have the ability to create your mortgage payment per month.